I was halfway through a long client call in my office overlooking Seattle’s waterfront when my phone buzzed with an unknown number, the kind I usually ignore because it almost always leads to a sales pitch or a mistake, but something about the persistence of the ringing made me pick it up anyway, and a measured, professional voice introduced himself as Andrew Collins, senior loan officer at Cascadia Federal Credit Union, asking me to confirm details on a home equity refinance that had apparently closed the previous afternoon on my property in Bainbridge Island, which immediately made no sense because I had not applied for any refinance, had not even considered touching that house, and for a moment I thought he must have dialed the wrong number, but when he calmly read the address aloud, I felt the ground under me shift in a way I could not explain, because that house was mine, the only real asset I owned outright, the one thing my grandfather had left me with a quiet instruction to “never let anyone talk you into giving it away.”

I stood up so abruptly that my laptop nearly slid off the desk, my voice sharper than I intended as I told him there had been no refinance and no authorization, and I could hear the pause on his end, the slight recalibration in tone that happens when a routine call turns into something else entirely, something serious, something procedural, and he lowered his voice just enough to signal that we were no longer in normal territory and asked if I could come into the branch immediately because there were documents he needed me to review in person, documents that, from the way he said it, already sounded wrong.

I barely remember grabbing my keys or shutting down my computer, only that I drove faster than I should have, missing turns, replaying his words over and over in my head, trying to construct a scenario where this made sense, but every version ended in the same place, which was that someone had done something with my property without me, and as I pulled into the credit union’s parking lot I felt a tightness in my chest that wasn’t panic exactly, but something colder, more precise, like the moment before you understand a problem you can’t undo.

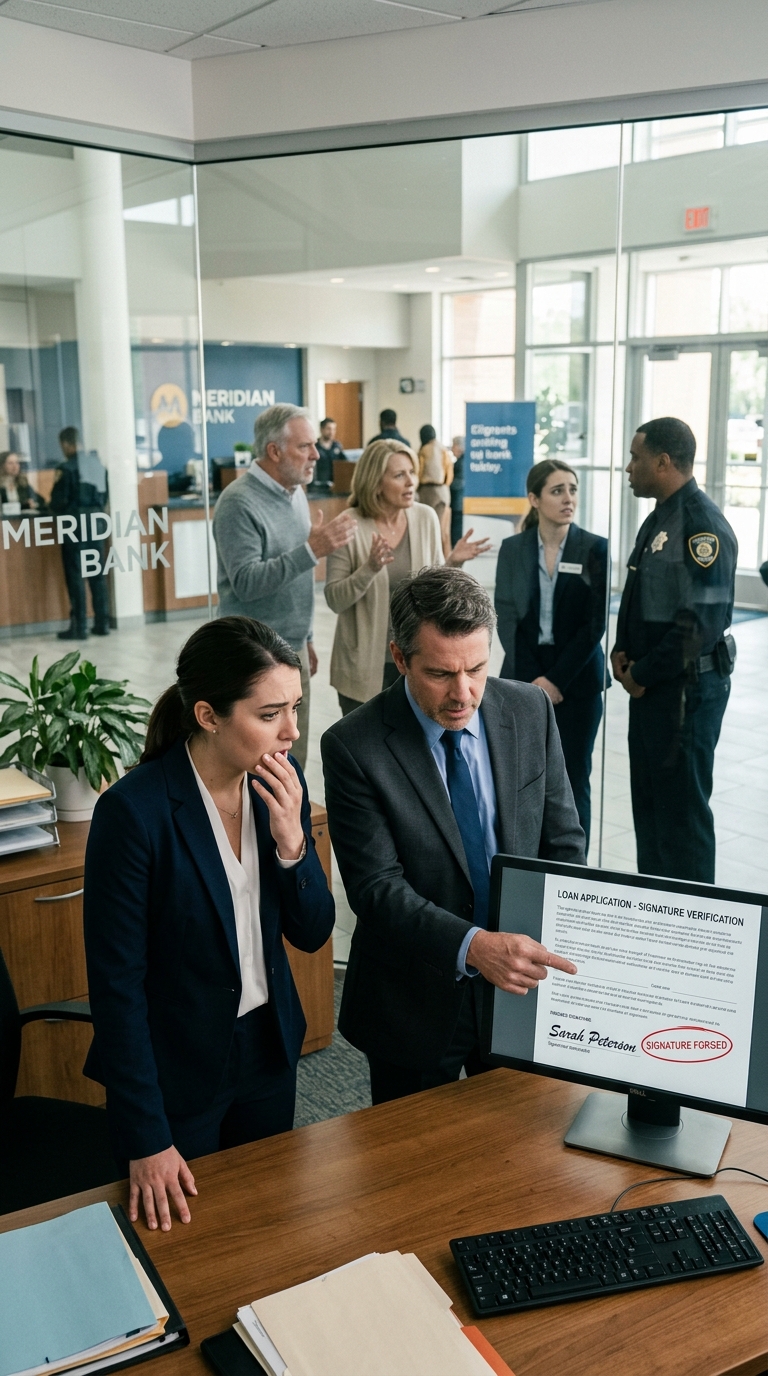

Andrew met me in a glass-walled office and closed the door behind us, his expression serious in a way that didn’t invite small talk, and he turned his monitor toward me, opening a digital file that showed a refinance agreement with my name typed neatly across the top and, more importantly, my supposed signature at the bottom, a signature that looked close enough to pass at a glance but wrong in the details, the slant off, the loops too deliberate, as if someone had practiced it slowly instead of writing it naturally, and I felt a strange clarity settle over me because I knew instantly it wasn’t mine.

“That’s not my signature,” I said, and Andrew nodded, already prepared for that answer, pulling up a previous document I had signed years earlier for comparison, placing them side by side in a way that made the differences obvious even to someone who wasn’t looking for them, and then he started clicking through the internal processing log, narrating quietly under his breath as he moved through each step—application intake, document upload, identity verification override—until he stopped abruptly, his hand hovering over the mouse as his face changed in a way that made my stomach drop before he even spoke.

“We’re freezing the loan immediately,” he said, more to himself than to me, then looked up and added, “Nothing has been disbursed yet, but we need to treat this as potential fraud.”

I leaned forward, my pulse loud in my ears, and asked the question that had already formed in my mind but that I didn’t want to say out loud because saying it would make it real, and he hesitated for a fraction of a second before turning the screen fully toward me so I could see the internal audit trail, where the employee authorization line listed a name I recognized instantly.

Megan Hart.

My aunt’s daughter.

My cousin.

The same Megan who worked in loan processing at this exact branch.

Before I could process that, voices rose outside the office, sharp enough to cut through the quiet hum of the building, and I turned to see my mother standing just beyond the glass, her posture rigid, her expression already defensive, with my stepfather just behind her and Megan slightly off to the side, clutching a folder like it could shield her from what was coming, and Andrew moved quickly to the door, stepping outside and closing it behind him, speaking to them in a low but firm tone I couldn’t hear, while my mother pointed at me through the glass with the kind of certainty that said she still believed she was in control of this situation.

Andrew came back in and locked the door, his voice now entirely procedural as he told me we needed to document everything, that I would have to sign a sworn statement confirming I had not authorized any refinance or granted power of attorney, that compliance and possibly law enforcement would be involved, and I nodded because there was nothing else to do, my hands steady even as everything inside me felt like it was shifting into a new configuration where trust was no longer a given but a variable.

The next hour blurred into forms, questions, identity checks, and printed stills from security footage that showed my mother and Megan sitting across from a loan officer, sliding documents across the desk, leaning in close as if proximity could replace legitimacy, and there was no image of me because I had never been there, never signed anything, never agreed to any of it, and yet my name sat on every page as if it had.

When the compliance officer arrived, the questions became sharper, more detailed, tracing back through every possible point of access, asking whether I had ever shared personal information, whether my family knew enough about my finances to impersonate me, whether I had ever signed blank documents or given informal consent that could be misinterpreted, and each answer tightened the picture rather than loosening it, because the truth was simple and therefore damning: I had said no, repeatedly, and they had decided that my no didn’t matter.

My phone started ringing nonstop, first my younger brother insisting that I was overreacting, that this was just a temporary measure to help stabilize a failing business, that everything would have been paid back, that I was “blowing up the family” over paperwork, and I remember standing there listening to him and realizing that, to him, the line hadn’t been crossed at the moment of forgery but at the moment I refused to accept it.

By the time I left the bank that evening, I had filed a formal fraud affidavit, met with a detective who explained the legal implications in clear, careful terms, and watched my mother try to frame the situation as a misunderstanding even as evidence stacked against her in ways that could not be explained away, and I didn’t go home that night because I no longer trusted the idea of access, not to my accounts, not to my space, not even to my sense of what was safe.

Over the next weeks, the investigation unfolded with a kind of methodical inevitability, revealing how Megan had used internal overrides meant for emergencies to bypass identity checks, how my mother had provided just enough information to make the application seem plausible, how a notary had stamped documents without witnessing a signature, and how the entire process relied on one assumption: that I wouldn’t find out in time.

But I had.

The loan was voided before any funds were released, Megan was terminated, charges were filed, and what remained was not just a legal case but the slow, complicated collapse of a version of my family that I had believed in long after it stopped being real, and in its place I built something quieter and more deliberate, setting boundaries that were no longer negotiable, protecting my property not just with paperwork but with awareness, and learning that trust, once broken in that way, doesn’t come back through apology or time but through consistent, provable change.

People ask if I forgave them, and the answer is not simple, because forgiveness, I’ve learned, is not the same as access, and I can wish them well from a distance while still refusing to give them the keys—to my home, to my finances, or to the version of myself that once believed they would never cross that line.